Fixed vs variable loan rates represent two very different paths in borrowing. Choosing the right type affects your monthly payments and overall savings. Understanding these options empowers you to make informed financial decisions.

Many borrowers find themselves confused between lock-in rates and floating rates. The distinction can influence your financial future significantly. Educating yourself on these loan types is crucial.

Don’t let uncertainty hold you back from making the best choice for your finances. Keep reading to discover which loan rate option can save you money!

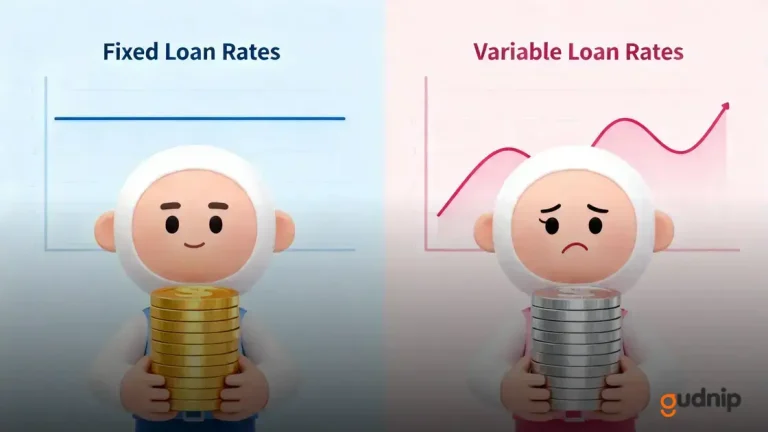

Understanding Fixed Loan Rates

Understanding fixed loan rates is essential for smart borrowing. Fixed loan rates keep your monthly payments the same throughout the loan period. This means you know exactly how much you will pay every month, making budgeting easier.

Choosing a fixed loan rate can be beneficial, especially if interest rates are low when you borrow. You lock in that rate, protecting yourself from future increases. This stability can give you peace of mind and make long-term financial planning simpler.

However, fixed loan rates can be higher than variable rates at the start. It’s important to weigh the pros and cons and consider your plans. If you stay in your home for a long time, fixed rates might save you money over time.

Understanding Variable Loan Rates

Understanding variable loan rates is important for anyone considering borrowing money. Unlike fixed rates, variable rates can change over time based on market conditions. This means your monthly payments can go up or down, making it a little tricky to plan your budget.

A main benefit of variable loan rates is the potential for lower initial payments. Because they often start lower than fixed rates, many borrowers find themselves saving money at the beginning. However, as interest rates rise, your payments could increase, and that may lead to higher costs in the long run.

It’s vital to think about your financial situation before choosing a variable rate. If you plan to stay in your home for a short time, a variable rate might save you money. But if you want stability, consider how fluctuating payments could impact your budget.

Pros and Cons of Fixed Loan Rates

Fixed loan rates have many advantages that can help borrowers feel more secure. One of the biggest pros is the stability they provide. Since your interest rate remains the same, you can easily predict your monthly payments. This makes it easier to create a budget and plan for the future.

However, there are also some downsides to fixed loan rates. They may start at a higher rate compared to variable loans. This means you could miss out on lower rates during economic changes. Borrowers who choose fixed rates might end up paying more in interest if market rates fall.

Despite the potential downsides, many people prefer the peace of mind that comes with fixed rates. It’s important to consider your personal financial situation when deciding. If you value consistency in your payments, a fixed loan rate could be the right choice for you.

Pros and Cons of Variable Loan Rates

Variable loan rates offer some appealing advantages for borrowers looking to save money. One major pro is that they usually start at lower rates compared to fixed loans. This can lead to lower monthly payments in the early stages of the loan, making it easier for borrowers to manage their finances.

However, the nature of variable rates comes with drawbacks. Since these rates can change based on market conditions, monthly payments can increase as interest rates rise. This unpredictability can make budgeting more challenging, leading to potential financial stress if rates go significantly higher.

Despite the risks, many borrowers appreciate the potential to save money with variable rates when the market is favorable. Balancing these pros and cons is crucial to making a wise decision. If you are flexible and can handle fluctuations, a variable loan rate might work for you.

How to Choose Between Fixed and Variable Rates

Choosing between fixed and variable rates starts with knowing your financial situation. Think about how long you plan to stay in your home. If you want stability and plan to stay for a long time, a fixed rate might be a better choice. This gives you peace of mind with your monthly payments.

Next, consider the current interest rates and your comfort with risk. If interest rates are low, a variable rate can save you money at first. But remember, rates can change, and that might lead to higher payments later. Make sure you’re okay with possible fluctuations in your budget.

Lastly, it helps to consult with a financial advisor. They can guide you through your options and help you understand what fits your needs best. Choosing wisely between fixed and variable rates can lead to better savings in the long run.

Impact of Interest Rate Changes

Interest rate changes can greatly affect your loan, especially if you have a variable loan rate. When interest rates rise, your monthly payments can increase, which might make it harder to stick to your budget. This can create financial stress, especially for families who need to manage their day-to-day expenses carefully.

On the other hand, if interest rates fall, those with variable loan rates could enjoy lower payments. This can lead to savings over time, as less money goes toward interest. It’s one of the reasons some borrowers prefer variable rates. However, the uncertainty of potential rises remains a concern for many.

For fixed loan rates, changes in interest rates won’t affect your payments. If you locked in a good rate when they were low, you might save a lot compared to current market rates. But, if rates drop after you borrow, you might miss out on potential savings. It’s essential to think about how interest rates can impact your choices when deciding on a loan type.

Long-term vs Short-term Loans

When considering loans, understanding the differences between long-term and short-term loans is vital. Long-term loans usually have repayment periods of several years, often up to 30 years. This means smaller monthly payments, which can help with budgeting. However, since you will be paying for a longer time, you may end up paying more in interest overall.

Short-term loans, on the other hand, are typically repaid in a few months to a few years. While this means higher monthly payments, the total interest paid can be less. Many people prefer short-term loans if they want to pay off their debt quickly and avoid long-term financial commitments.

Your choice between long-term and short-term loans should depend on your financial situation and goals. If you need lower monthly payments, a long-term loan might be the way to go. But if you want to save on interest and can handle higher costs, a short-term loan could be a better fit.

Analyzing Your Financial Situation

Analyzing your financial situation is a crucial step in choosing between fixed and variable loan rates. Start by looking at your monthly income and expenses. Understanding how much you can afford to pay each month will help you select a loan option that fits your budget. Creating a clear picture of your finances allows you to make informed decisions.

Next, assess your long-term financial goals. Do you plan to buy a house and stay there for many years? A fixed loan rate may provide stability and peace of mind. Alternatively, if you expect your circumstances to change soon, a variable rate could be more suitable, offering lower initial payments.

Finally, consider your comfort with financial risk. If you prefer predictable costs, fixed rates are likely the better choice. However, if you can manage possible changes in payment amounts, variable rates might offer initial savings. By carefully analyzing your financial situation, you can make a more confident choice.

Expert Advice on Loan Rates

When seeking expert advice on loan rates, it’s essential to consult a financial advisor. They can help you understand the current market trends and how they apply to your specific situation. Advisors often have valuable insights on the differences between fixed and variable rates, assisting you in weighing the pros and cons of each option.

Experts often recommend evaluating your long-term goals and financial readiness before deciding on a loan type. If you seek stability for the next few years, they might suggest a fixed rate. However, if you’re open to some risk and can handle potential rate fluctuations, a variable rate might offer initial savings.

Lastly, keep in mind that rates can vary between lenders. It’s wise to shop around and get quotes from multiple sources, as this can lead to better offers. Taking the time to gather expert advice and compare options can lead to more informed, beneficial decisions regarding your loan.